|

The funding formula is the key parameter used to

assess institutions’ needs. But in finalising its funding recommendations, the UGC also takes into account the

special needs of individual institutions and other factors not captured by the formula and will introduce extraformulaic adjustments where required.

Earmarked grants for specific purposes are allocations outside the block grant system. Examples are the

earmarked research grants, grants for knowledge transfer activities, and grants for areas of excellence scheme.

Once determined, recurrent funding for a triennium will not be adjusted during the period except for adjustments

to take into account changes in the indicative tuition fee levels, new initiatives from the Government and

civil service pay adjustments.

Following the civil service 2009 pay cut and 2010 pay rise which took effect

from 1 January 2010 and 1 April 2010 respectively, the subvention for 2010/11 was reduced by approximately

$220 million.

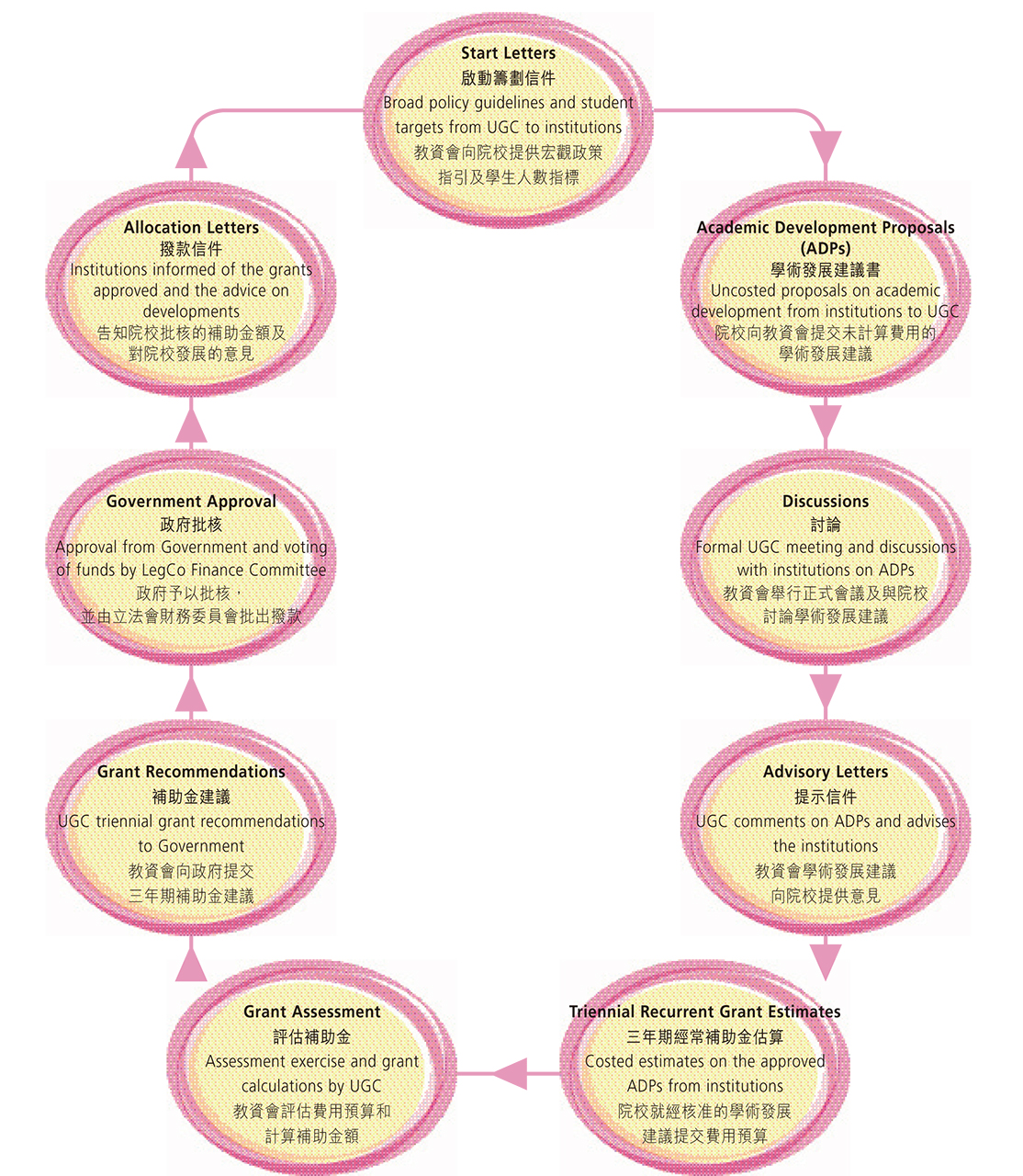

| Diagrammatic Illustration

of UGC Recurrent Grant Cycle

|

|

|

Financial Reporting

and Monitoring

The UGC-funded institutions are autonomous statutory

bodies governed by their respective Ordinances. They enjoy institutional autonomy in such areas as curriculum

design, selection and recruitment of staff and students, and internal allocation of finances. While respecting the institutional autonomy of our funded institutions in

allocating and managing their internal finances, the UGC adopts an accountable and transparent approach in

ensuring the public money entrusted to the institutions are applied meaningfully and provide value for money.

To provide institutions with substantial financial freedom,

the bulk of the subvention to institutions are in the form of the block grant, which provides for a “one-line” allocation

of resources for a funding period (usually a triennium) without prescription attached as to how it should be spent. The major requirement is that such grant must

be used within the ambit of “UGC-fundable activities” while adhering to approved student number targets. The

precise amount of the block grant has to be approved by the Finance Committee of the Legislative Council

before the start of every triennial funding period, after which the responsibility falls squarely upon the institutions to apply

those funds appropriately.

•

Institutions are accountable for any unspent

balances of the public funds

While being entitled to maintain a general reserve

of up to 20% of the institution’s total approved recurrent grants (excluding any earmarked grants) in

a triennium for future and new development needs, any excess of that level has to be returned to the

UGC. The use of the general reserve is subject to the same rules and regulations governing the use of

recurrent grants. For grants earmarked for specific purposes, any amount unspent after the close of

financial year or approved funding period must be returned.

•

Institutions provide regular reports on their

finances to the UGC

We require institutions to submit for each financial

year an annual return on the use of all UGC funds. We also require Heads of Institutions to provide a

Certificate of Accountability to the UGC annually to confirm that the public funds allocated via the UGC

have been spent in accordance with the rules and guidelines as agreed with the UGC.

•

No cross-subsidisation of UGC resources to

non-UGC-funded activities

Recurrent grants are provided to the UGC-funded

institutions to support their academic and related activities based on approved UGC-funded activities.

As such, there should be no cross-subsidisation of UGC resources to non-UGC-funded activities

(including, but not limited to, self-financing activities). To avoid hidden subsidy to non-UGC-funded

activities, the institutions should levy overhead charges on such activities, including projects funded

by other Government departments/agencies and projects/programmes conducted by their selffinancing

subsidiaries or associates.

•

Institutional finances are subject to professional

accounting standards and external audit processes

Institutions are required to keep proper accounting

records in accordance with the Hong Kong Financial Reporting Standards and the house guidelines on

recommended accounting practice adopted by the UGC where appropriate. Institutions also arrange

their own external annual audits on their financial statements and the annual return, in accordance

with prevalent assurance engagement standards adopted by the audit profession. For the purpose

of efficient use of public funds, institutions are also subject to examination by the Director of Audit.

•

Financial affairs working Group

From time to time, the UGC may express interest in

the financial well-being of UGC-funded institutions and enquire on specific financial issues concerning

the UGC sector. To strengthen the financial monitoring effort, the UGC established a new

Financial Affairs Working Group in January 2011 with professional expertise to work with institutions

to help ensure their continuing good financial governance and sound financial planning.

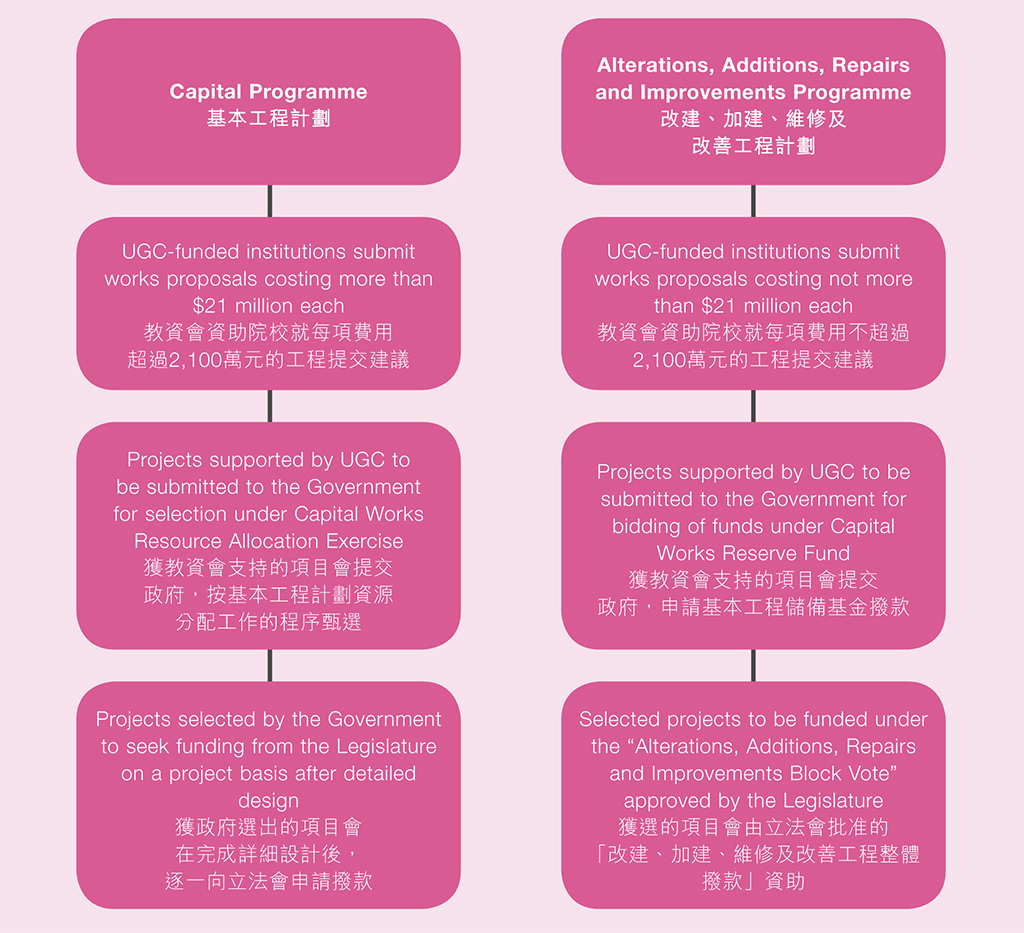

Capital

Grants

The UGC supports capital works projects of institutions

for UGC-approved activities by capital grants sought from the Government on an annual basis under the Capital

Programme, and the Alterations, Additions, Repairs and Improvements Programme. Details of the two capital

grants programmes are illustrated in the flowcharts below:

In 2010-11, there are 26 ongoing capital works projects

under the Capital Programme with a total estimated project cost of some $12 billion. The expenditure on

these projects in 2010-11 was about $1.8 billion. With the commencement of superstructure works of most projects,

the spending in 2011-12 is anticipated to increase to some $3.6 billion.

In 2010-11, the UGC supported a total of 32 new Alterations, Additions, Repairs and Improvements projects

submitted by institutions with a total estimated cost (to be spread over up to three years) of some $530 million.

To meet the expenditure of the ongoing and newly approved projects in 2010-11, a total of $270 million was

allocated to institutions. The allocation will be increased to some $440 million in 2011-12 as institutions carry out major

spatial reorganization works to prepare for the new four-year academic structure.

|

CityU’s newly completed Multi-media Building

|

Improvement works to Joint Sports Centre

|

|

Major renovation and upgrading of the lecture theatre at Shaw

Campus of CUHK

|

Construction of food courts and multi-purpose area

at covered podium of Haking Wong Building of HKU

|

Financial Reporting

and Monitoring

The capital grants are charged to the Capital Works

Reserve Fund and are part of the Capital Works Programme of the Government. Institutions’ projects

under capital subvention follow the procedures for creating and managing a capital works project under the Capital

Works Programme. Institutions assume full responsibility and accountability for their projects under capital subvention. They ensure that works expenditure stays

strictly within the approved project estimate in accordance with the approved project scope i.e. the scope approved

by the Legislative Council for capital works projects exceeding $21 million, and the scope approved by the

UGC for Alterations, Additions, Repairs and Improvements projects up to $21 million.

Institutions have in place an appropriate system of cost control and monitoring mechanism for overseeing the

spending of public money having regard to economy, efficiency and effectiveness in the delivery of their

projects. In particular, institutions ensure proper procurement procedures are in place, taking reference

from Government’s latest rules and regulations applicable to public capital works.

Approved funds for the projects are released to the institutions on a monthly basis. Institutions are required to

submit a monthly statement on the financial position and a quarterly report on the progress of their projects. Upon

completion of a project, the institution should submit a statement of final accounts to the UGC and return

any unspent balance or unapproved expenditure to the Government.

Streamlining Administrative Procedures

Last year, the UGC embarked on a thorough exercise

to critically review the Notes on Procedures – a long established document setting out the functions and

responsibilities, regulatory matters, and the interplay among the Government, the UGC and all the funded

institutions – and eliminated unnecessary administrative procedures on a wide range of major areas, among which

is the streamlining of procedures for capital grants, and removing the requirement of seeking UGC’s approval on

major equipment purchases. We believe such revisions will considerably reduce the administrative burden of

institutions and the UGC, while enhancing the clarity of the ambit of each party’s responsibilities.

|